Student Loan Forgiveness: What's Next?

On Wednesday, August 24th, President Biden announced his administration’s Student Loan Debt Plan. This news may bring up questions for you, and we are here to answer them.

Here are the Details you Need:

Who qualifies for loan forgiveness?

Federal student loan borrowers who earn less than $125,000 per year or married couples who make less than $250,000 per year on their 2020 or 2021 tax return.

Private and Federal loans taken after June 30th, 2022, are not eligible.

How much will be forgiven?

$10,000 of student loan debt is canceled for all federal student loan borrowers.

An additional $10,000 ($20,000 total) of student loan debt is canceled for those who received Pell grants.

How can you ensure you receive forgiveness if you qualify?

Borrowers who are already on income-driven repayment plans will automatically receive forgiveness. The Department of Education will make an application available during the month of October. Due to high-volume traffic, the application and income verification process will likely take time.

Borrowers can sign up for updates from the US Department of Education to be notified when the application becomes available by clicking here.

Other key dates to remember:

November 15th The deadline to apply to receive debt cancellation by the time the payment pause expires at the end of the year. Your application must be submitted by November 15th.

January 1, 2023: If you didn’t receive total forgiveness, payments will start back up and interest will begin accruing on the balance on January 1, 2023.

December 31, 2023: The final deadline to apply for student loan forgiveness.

Forbearance extension

Biden also extended the pandemic student loan forbearance that was set to expire on August 31st to the end of the year. This will benefit those who won’t qualify for forgiveness and those who will still have a balance remaining after forgiveness.

Proposed change of repayment based on income: Those with undergraduate loans who are on income-driven payment plans, may be able to cap repayment at 5% of their monthly income. This is half of the current rate most borrowers pay now.

How does this affect Your current financial situation?

This news will likely create further questions regarding your specific financial landscape. Here are a few examples of how this change is applied to everyday people:

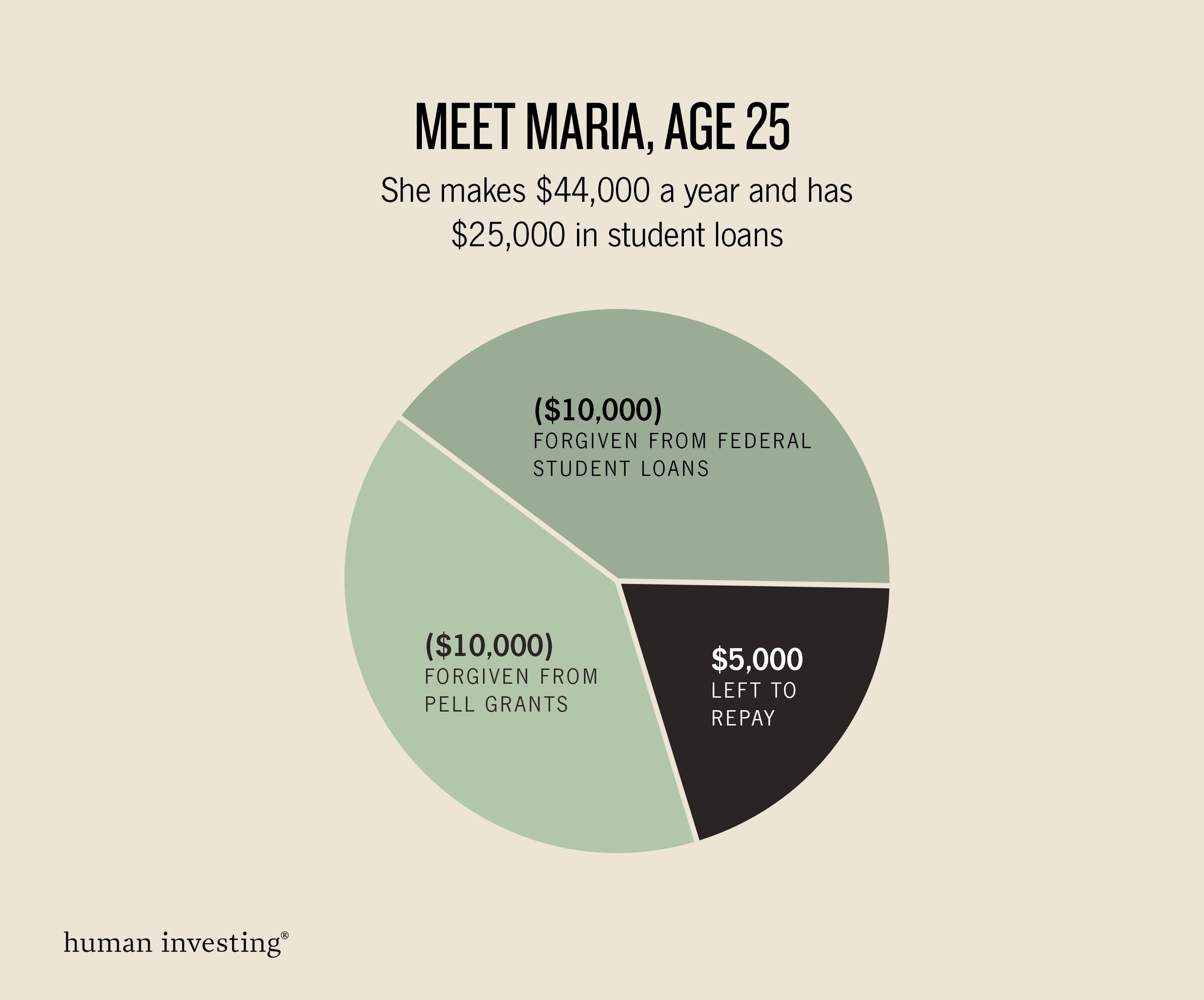

MARIA, AGE 25

Maria graduated in 2019 with $25,000 in student loan debt and currently makes $44,000 per year. One of the loans she received was a Pell Grant. According to Biden’s plan, Maria will only have $5,000 left to repay starting in January 2023.

ANDREW & MONICA, AGE 43

Andrew and Monica are a married couple. Together, they carry $40,000 in student loan debt and make a combined income of $260,000 per year. Due to their income, they are ineligible to receive student loan debt forgiveness and will need to resume their repayments starting in January 2023.

SEAN, AGE 35

Sean graduated in 2017 with $8,000 in student loan debt and currently makes $75,000 per year. All of Sean’s student loans are canceled, with no repayments resuming in January 2023.

How Should You Adjust Your Financial Plan?

However you are receiving this news, you should use this opportunity to assess your finances and take action to get closer to your long-term goals. Here are a few tips:

If your student loan debt has been altogether canceled:

Take some time to reassess your spending and saving habits – create a budget.

Bolster your emergency savings fund: Make sure you have 3-6 months of expenses saved.

Use the extra cash to pay off any consumer debt.

If you have no consumer debt and have extra cash, consider redirecting those repayments to funding a Roth IRA. (Up to $6,000, or $7,000 if you are aged 50+).

Reconsider short-term and long-term goals.

If your student loan debt repayments are resuming in January 2023:

Edit your budget to include these payments.

Consider restarting your monthly payment schedule. This will save you money in accrued interest by paying down the principal during the payment pause.

As always, our team at Human Investing is here to help should you have any further questions. If you would like to talk with an advisor, call 503-905-3100.