The Dangerous Reality Of Using Your 401k To Finance Your Vacation.

Looking to go on a “once and a lifetime” vacation to Fiji? Renovate your kitchen? Upgrade your car? Did you know you may be able to utilize your 401k or other retirement plan to take a loan to help finance this big expense? Here are the details, the dangerous reality, and things to consider when taking a 401k loan:

The Details:

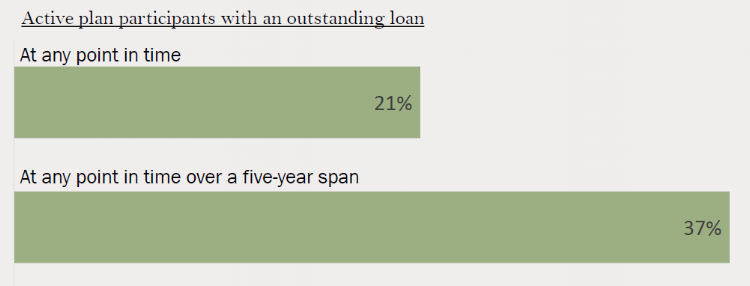

If your plan document permits, a 401k loan can help you access up to $50k of likely your biggest pool of assets, avoid creditors, pay interest back to yourself (typically prime rate + 1%) and there is no need for good credit to qualify. You wouldn’t be the only one taking advantage of this opportunity; according to the National Bureau of Economic Research, about 1 in 5 active participants have a 401k loan.

NBER Working Paper No. 21102

The Dangerous Reality:

Does all of this sound too good to be true? Well, it just might be. A 401k loan can come at the cost of hundreds of thousands of dollars in future retirement income (see graph below). So, whether you have a loan or are planning to take a loan, it is important to know some of the dangers of borrowing against your future self:

Forfeit the tax advantage of your retirement plan dollars - When you are paying back your loan, interest payments are done so after tax. This forfeits the tax advantage of these retirement dollars as taxes are paid when you contribute and later withdraw.

Leaving your employer? Think again - If you leave employment at your company, whether by your choice or your employer’s, you will find yourself in a sticky situation. The remaining balance of the loan will need to be paid back by the time you file taxes for the current year. Defaulting on your 401k loan comes at a great cost. The remaining loan balance will be considered taxable income. If you are under age 59 ½, a 10% early withdrawal penalty will be tacked on as well.

Abandon free money – If your 401k has an employer match you may miss out on free money if you cannot afford to continue contributing to your 401k while paying back the loan.

Miss out on market growth - Your dollars are not fully invested while you have an outstanding loan balance. This means a portion of your portfolio would miss out on opportunity for growth, specifically when market returns are greater than the interest rate paid to yourself.

Detrimental impact on retirement income - A 401k loan can have a detrimental impact on your retirement savings and your potential income in retirement. The below graph shows the effects on an individual’s retirement savings and monthly retirement income. Three scenarios shown are 1) take a 401k loan and push pause on contributions; 2) take a 401k loan while continuing to save; and 3) don’t take a loan.

This graph is for illustration purposes only. It highlights the impact a loan has on an individual’s retirement balance and monthly retirement income after 30 years of investment growth during working years (assuming 7% annual market return and annual contributions of $7,500) and 30 years of income through retirement (assuming 4% rate of return). In this example an individual takes a $15k 401(k) loan from a $50k balance to pay down some bills and a finance a vacation.

The “once in a lifetime trip to Fiji” can ultimately cost more than $1,400 per month in retirement income.

That’s $515k over 30 years of retirement!

Options to consider:

For some, a 401k loan can be a helpful tool when “life happens,” allowing participants of retirement plans the ability to access a pool of assets intended for retirement. However, while this can be an attractive tool for some, borrowing from your future self can have its drawbacks. Either way, here are issues worth thinking about:

Want to go on a once in a life time trip to Fiji, or finance some other big expense that isn’t worth putting your retirement income in risk? Budget for future big expenses, plan and start saving today.

Building an emergency reserve (3-6month’s income) to keep you on track financially and avoid a last resort 401k loan when an unexpected expense comes up.

Are you in a pinch and need to take a loan or have already taken a loan? Continue saving in to your retirement account so as to not miss out on valuable retirement savings and possible employer match.

Want to take a 401k loan? Check with your HR representative or 401k advisor to see what options are available to you.