2023 Q4 Economic Update: Labor’s impact on the economy

In recent months, I’ve been pondering the US labor force and how it has changed in the last five years. Amid the ongoing conversations surrounding inflation and the Federal Reserve's (aka The Fed) recent decisions to raise interest rates to manage inflation, I don’t want to neglect the other part of The Fed’s dual mandate: the dynamics of unemployment and the labor force. Prior to COVID-19, unemployment was at 3.5%, the lowest rate in the last 50 years. Today unemployment is around 3.8%, and has been 4% or lower since December 2021, significantly below the median unemployment of approximately 5% the US has experienced over the last 25 years. Since March 2021, job openings have consistently surpassed the number of job seekers.

Unemployment is often considered an indicator of an economy’s health. Like inflation, you want some unemployment, but not too much. Too high unemployment indicates a weak economy. If unemployment is too low, high inflation becomes a concern. Businesses seeking to grow may be constrained because of a lack of workers, limiting overall economic growth.

Strong employment is a major reason why 2023 has not experienced the recession that many feared at the beginning of the year. I wanted to delve into the reasons behind the tight labor market, what can be done about it, and what this signifies for the overall economy.

Labor’s impact on the current economy

The fundamental assumption in most economic models is that production is constrained by two primary inputs: labor (i.e. workers) and capital (i.e. technology). While technology has yielded significant advances in productivity, the necessity for a workforce to drive economic growth remains. A shortage of labor would imply slower economic growth, potentially resulting in reduced stock market growth.

Concerns persist regarding automation displacing jobs. Some have even proposed the implementation of a universal basic income due to the scarcity of employment opportunities resulting from automation (as exemplified by former presidential candidate Andrew Yang, who made this a central theme of his campaign). A variation of this concern has been present for over a century.

The latest development in automation centers around AI potentially increasing productivity to the extent that we might encounter a surplus of labor. Numerous case studies illustrate that technological change does not always materialize as successfully or rapidly as initially projected. A decade ago, there was much buzz about how autonomous cars were poised to revolutionize the world. Substantial progress has been made, but the challenge of perfecting driverless cars has proven more intricate than many had anticipated. (An example is Moral Machine, where you weigh in on how a self-driving car should navigate situations where the car must choose who to protect in an unavoidable collision).

Another illustration can be found in the excessive optimism at the peak of the dot-com bubble. While the internet did transform the way we work and introduced new efficiencies, it took significantly longer than what people in 1999 had envisioned. Forecasting the timeline for technological change impacting worker productivity is challenging.

If I had to guess, I would anticipate that in the near term (i.e. the next 5 years), we will continue to experience a tight labor market that will be a headwind to growth, for the economy and the stock market.

Retiring baby boomers present a significant challenge

By 2030, the youngest Baby Boomers will turn 65. The average American retires at 64. These retiring Baby Boomers possess the most expertise and would ideally be succeeded by Gen X workers with slightly less experience. However, Gen X is too small of a generation to fully replace the baby boomers, and Millennials & Gen Z broadly lack the experience necessary to fully replace the skills of retiring baby boomers.

This is backed by recent projections by the Bureau of Labor Statistics (BLS), showing that total employment is expected to grow by only 0.3% annually for the next decade, with a significant constraint being the slower growth of the working age population. Slowing growth in labor likely means slowing growth in GDP and stock prices.

Furthermore, there has been a consistent decline in the labor force participation rate over time. This is a measure of everyone 16 and older who is not in the military or an institution (due to criminal activity, mental health, or aging). Part of this reflects the aging population. As the proportion of the population beyond retirement age increases, a smaller segment of the population remains in the workforce.

How can we increase labor?

Gen Z is entering the workforce, but as a generation, they are too small to completely replace retiring baby boomers. Producing more working-age adults takes at least 16 years and 9 months, and the US birthrate has been below the stable replacement level of 2.1 for most of the last 50 years. If the US wants to sustain long-term population growth, and consequently, workforce expansion, it must either depend on immigration or find ways to boost the birth rate.

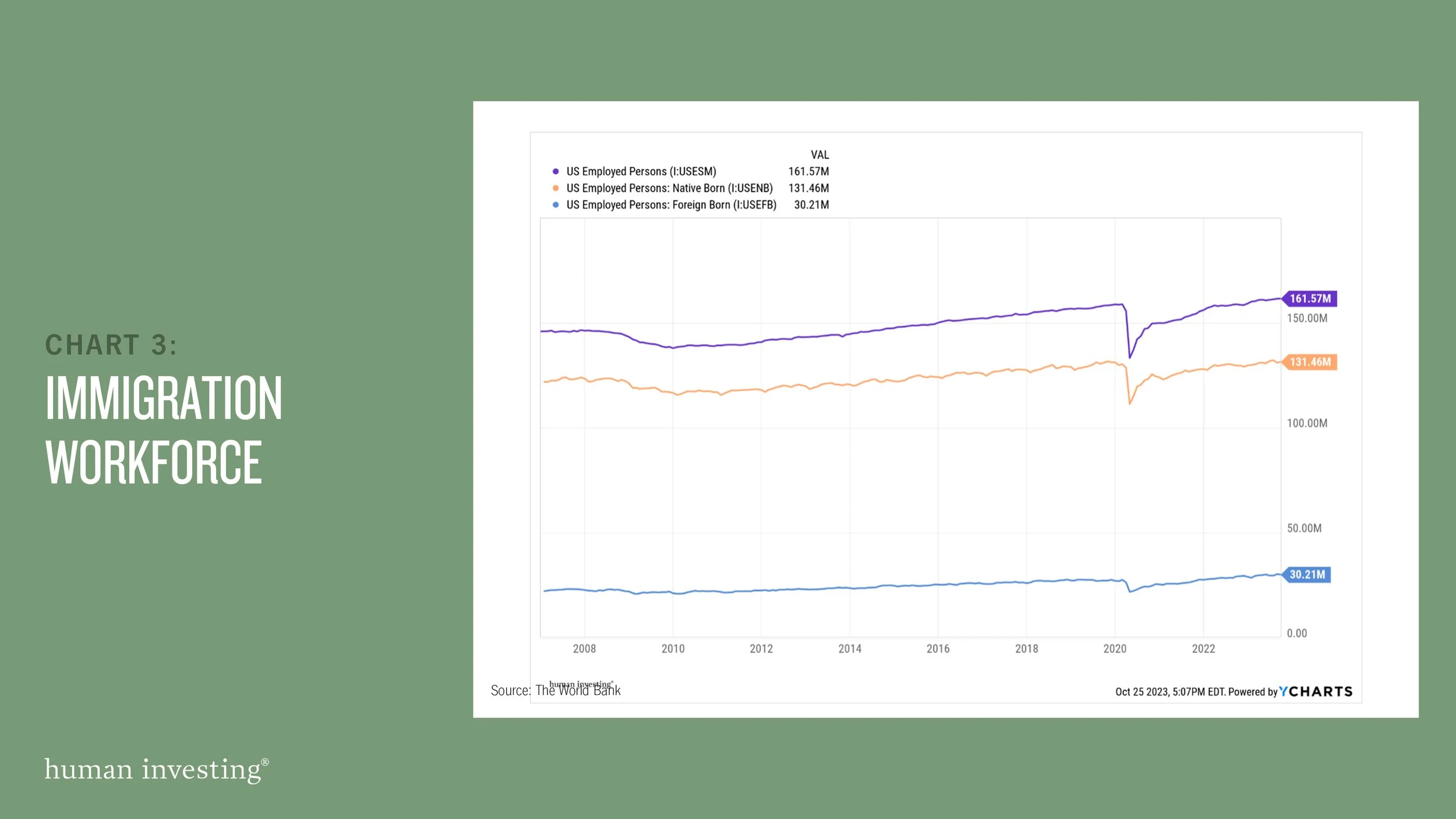

Implementing a policy permitting increased immigration could boost the size of the workforce in America. However, this is a politically contentious issue, and the legal framework around immigration is too uncertain to make reliable long-term predictions. Overly restrictive immigration policy could lead to a labor shortage, and too permissive immigration policy could cause a labor surplus. Foreign workers constitute approximately 20% of the US workforce.

A tighter labor market has some benefits for workers

The scarcity of labor translates into more choices when seeking employment and enhances the bargaining power of job seekers. Companies will have to consider their recruitment and retention policies to ensure they have the workers required for optimal performance. US wages and salaries are remaining above inflation, showing workers ability to demand higher compensation.

A tighter labor market plus higher wages could equal higher inflation rates

However, higher wages also entail increased costs for companies, and the allocation of these costs, whether to customers or shareholders, may result in higher inflation or reduced earnings. To counter inflation, the Federal Reserve has been increasing and maintaining higher interest rates. Many are apprehensive that the tight labor market (associated with demand-pull inflation) and ongoing post-COVID supply chain challenges (linked to cost-push inflation) could make achieving the long-term target of 2% inflation more challenging.

In Q3 2023 we observed inflation rates increasing from just below 3% in June to 3.7% in September. Many consider unemployment and inflation to have an inverse relationship. A tighter labor market may necessitate the Federal Reserve to persist with a more extended and aggressive tightening policy to manage inflation. If the Federal Reserve becomes overly aggressive in its tightening efforts, the concerns that led many to anticipate a 2023 recession could materialize.

All of this hinges on the tight labor market persisting. Technological advancements have the potential to enhance productivity to a level where a smaller workforce can achieve more and sustain economic growth. Modifications in immigration policy could either introduce a new source of workers or further reduce the size of the workforce.

In the long run, successful companies will adapt to the new environment and thrive. A diversified portfolio will continue to capture the growth of the companies that excel. We encourage investors to be prepared for a myriad of reasons to be nervous, and understand given time the market will figure things out and continue to grow.