Financial Planning: A Solution for Market Volatility and Loss Aversion Bias

In order to achieve retirement readiness, financial planning should be the focus of most individuals and families. Indeed, knowing how much a household needs to save and invest in producing a suitable level of income at retirement makes much sense. At the same time, given the recent uptick in market volatility, I have noticed additional benefits. Clients who have gone through the financial planning process appear to be at greater peace with the stock market gyrations. Further, when focused on executing their plan and not mentally tethered to the markets, clients are less prone to letting their behavior negatively impact their long-term performance.

Much of the time, financial planning does a great job of identifying how much an individual or family should own in both "safe" and "risk" investments to meet short-term cash and safety needs, as well as long-term growth objectives. In the absence of a financial plan, investors are left to wonder if they have the right mix of investments. Moreover, when market volatility increases, they are often the first to let their emotions get the best of them. Absent a financial plan; the focus is on the stock market. If the focus is on the stock market, and the market is temporarily going down, the pain of the volatility or what psychologists call "loss aversion bias" is too much to handle. As a result, at exactly the wrong time and for the wrong reason, we get a call to "sell everything" locking in those temporary losses—only to see the market recover as the investor sits on the sideline wondering when to get back in. Selling into a market that is going down is a significant reason investor returns and market returns are so different.

Dalbar, Inc. tracks investor return versus market returns, and the results are eye-opening. Our observation is that much of the gap between the long-term investor return and the long-term market returns are due to poor behavior and investors lacking a financial plan. In our view, having a financial plan is paramount as it gives a leg up to investors in two ways: 1) it helps center the discussion about money around goals and 2) it allows investors to minimize their dependence on monthly, quarterly, and annual stock market swings while redirecting the discussion back to goals-based planning. Goals-based planning is just a discussion on how many dollars will be needed and in what timeframe—this process alone will help determine the amount of safe versus risky investments.

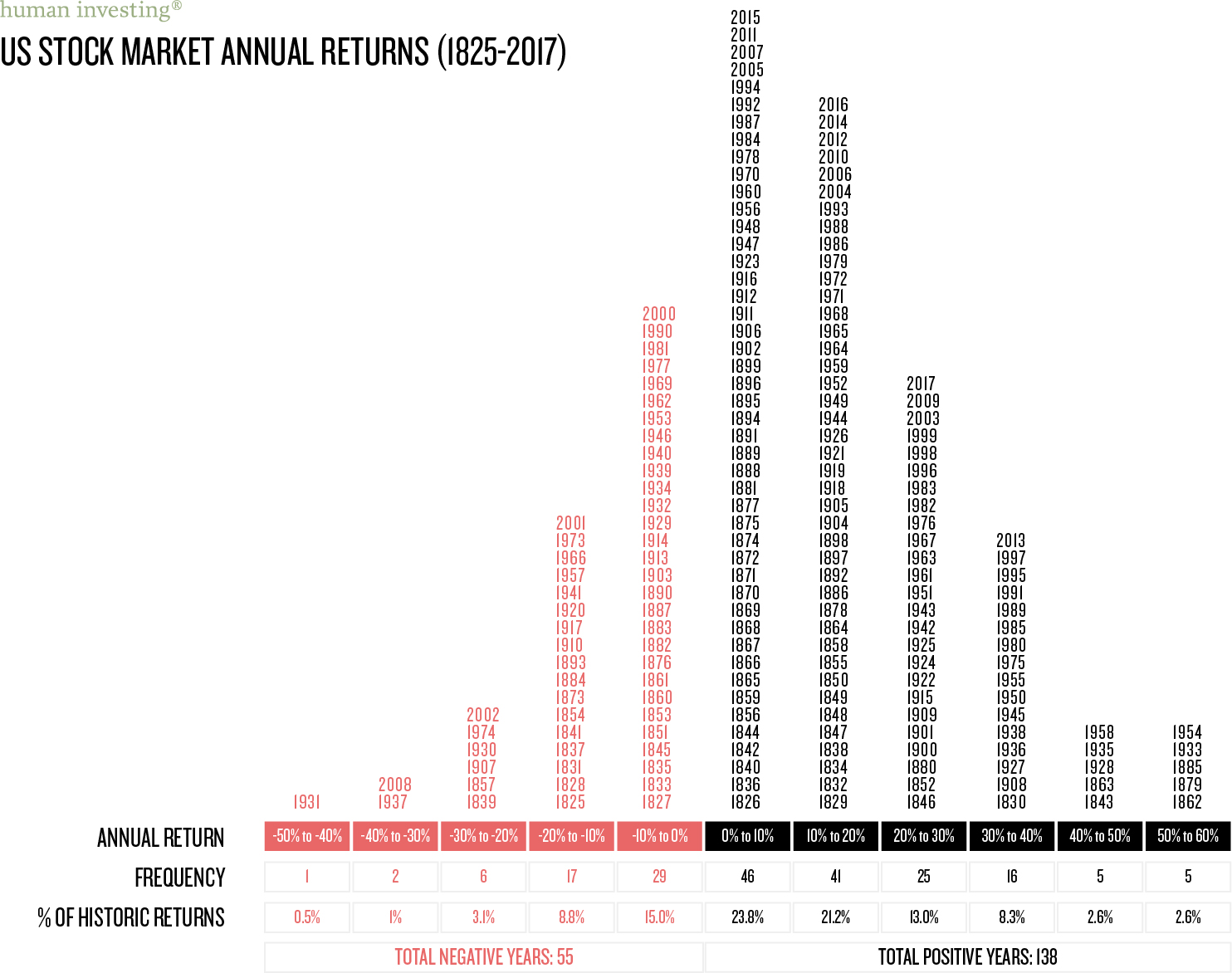

Finally, comprehending the odds of success or failure in the market may be a massive help in keeping nerves at bay and focused on the things that matter most. Although the legal language would point us towards a statement about past performance being no indication of future success, we can look at the distribution of returns in the stock market going back to 1825 and feel very good about the chance of a positive outcome. It all adds up to 71.5% of the time the stock market has been favorable, in spite of many ups and downs in between.