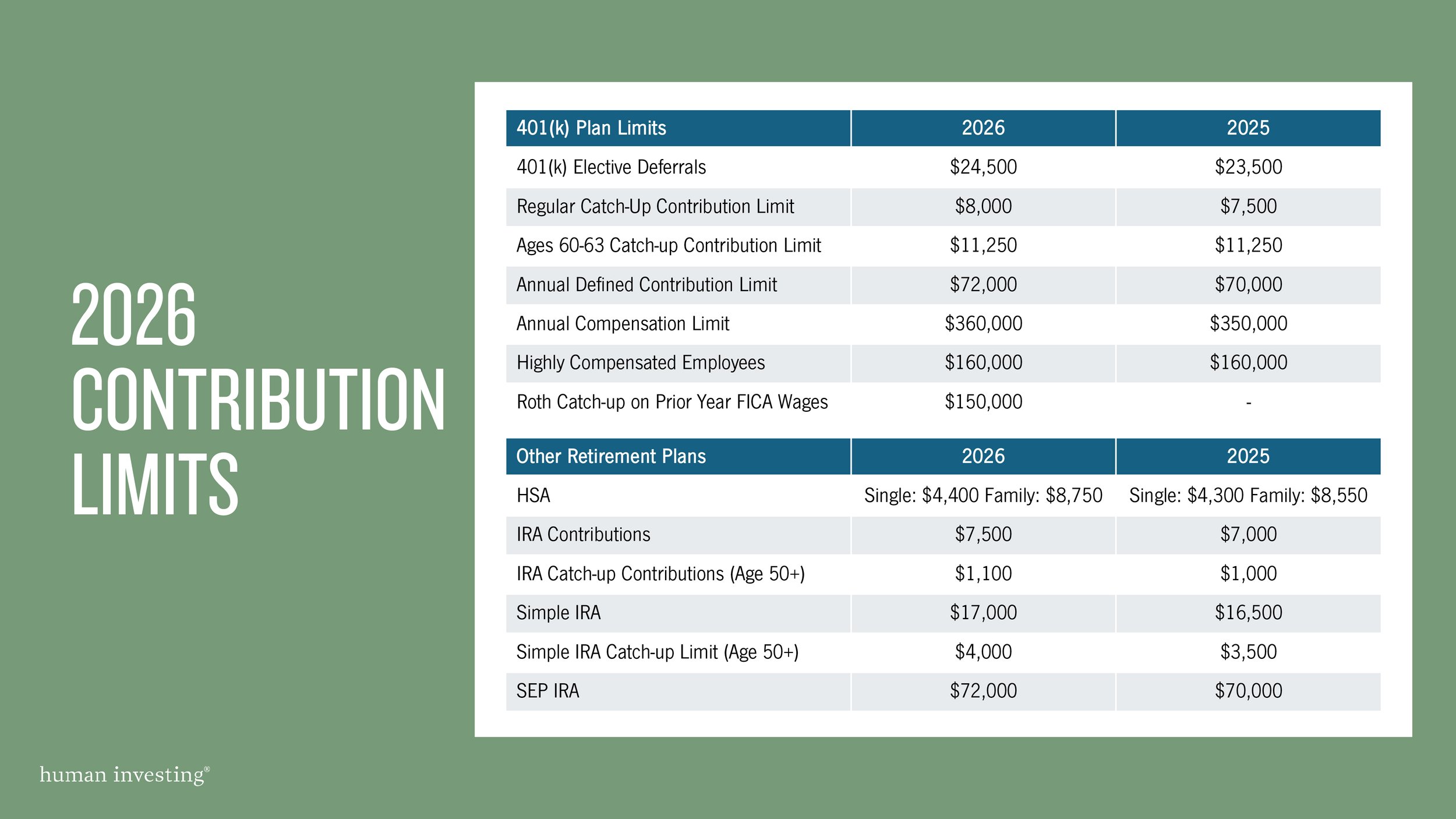

401(k) Investing Series: Analyze your company's investment lineup with this framework

Corporate retirement plans (401(k), 403(b), 401(a), 457(b), etc.) made up a total of $12.2 Trillion as of March 31, 2025. It goes without saying that these types of accounts make up a significant portion of how Americans save for retirement. In this series we want to help equip and educate investors on how to successfully navigate selecting their investments, sticking to a game plan, and ultimately growing their account in the most efficient way possible.

What matters the most

Asset Allocation

Luckily, studies have been done and papers have been written about the number one determinant of portfolio success. As the pie chart below shows, allocating funds appropriately across asset classes is BY FAR the number one factor that determines portfolio success.

Put differently, ensuring that an investor selects a fund (or funds) that diversifies their investments will outperform the investor who spends time on trying to time the market or ensure that the security they selected is superior to other investments in the same peer group. This can be accomplished using a Target Date Fund, Target Risk Fund, Model Portfolio, or by creating a custom asset allocation.

Expense Ratio (or Fund Cost)

The next variable that we would say matters most is ensuring that the fund or funds you select has a low expense ratio. What’s low? In 2024, the average expense ratio for an index fund was 0.05%. In our opinion, if the index fund you select has an expense ratio of less than 0.15% we think you are checking the box on selecting a low-cost option.

What matters less

Historical Performance

Talking about historical performance is no easy task. The point here is that when you are on your retirement plan website and looking to learn about the investment options, the majority of the information is about the performance of the funds. And while that information might stand out the most, it’s actually not the most helpful. We think about fund performance track records in this framework:

Asset class performance is more important than actual fund performance. More specifically, owning the Large Cap asset class is more important than trying to select a specific large cap manager.

So much can go into why a specific fund performed well or did not perform well over the last 1 year, 3 year, 5 year, or 10 year performance period. Only looking at these variables has not been a good indicator of if a fund is going to perform well on a go forward basis. A majority of the top-half performing funds fall out of the top half after 5 years.

Our recommendation, if you are going to look at funds in a more in depth way look at variables like risk-adjusted return or the specific track record of the management team. Another option is to simply select a low-cost index fund.

A visual guide on what to look for

We created this table to help provide a road map for selecting investments. This sample fund menu contains; investment options, historical performance, cost, and if the fund should be used on a stand-alone basis (provides ample asset allocation) or should be held alongside other investment options.

Want to talk about your company’s retirement plan?

Schedule time to meet with an advisor below or e-mail Andrew at andrew@humaninvesting.com.