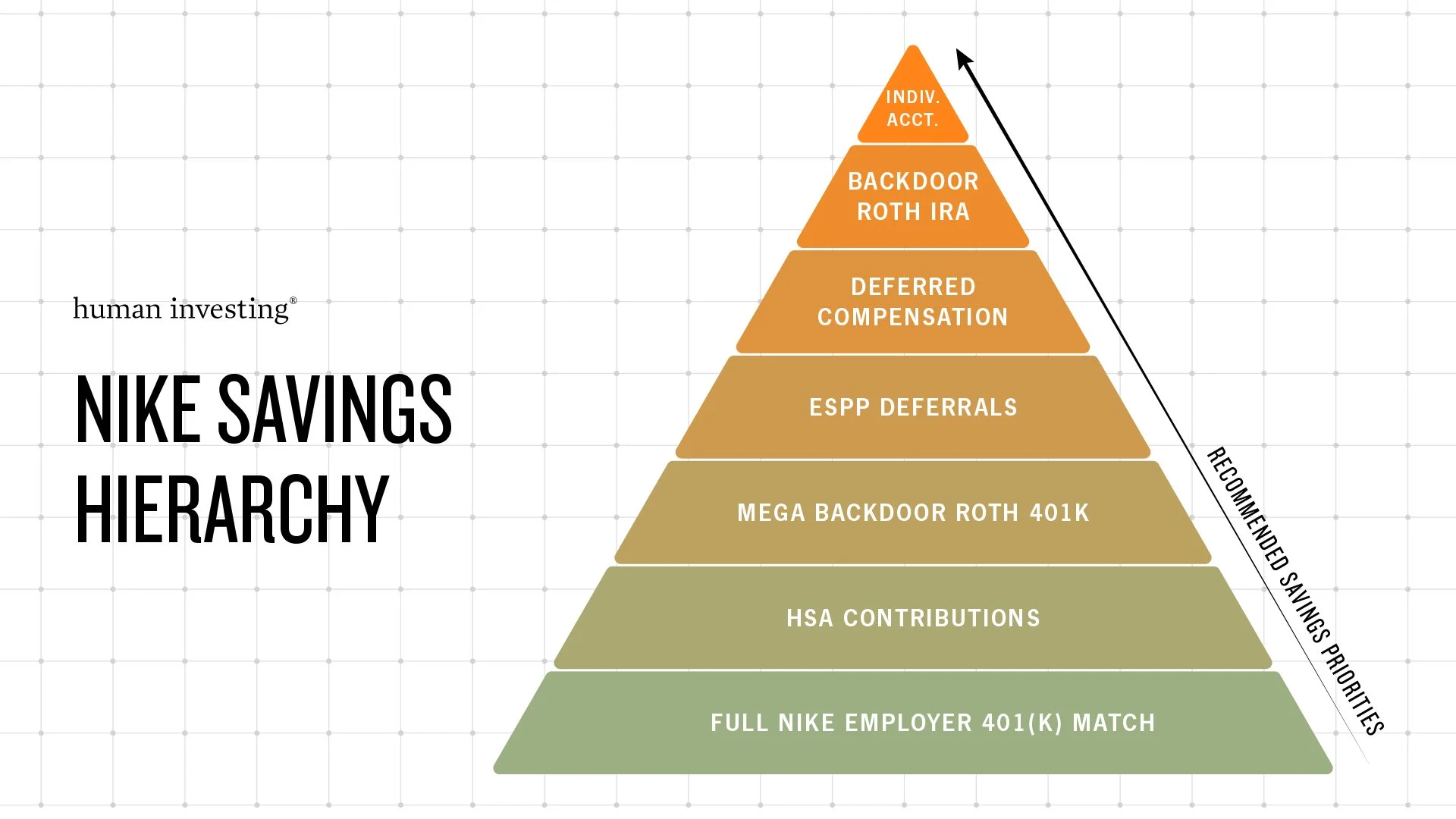

The most underrated Nike benefit: The Health Savings Account

As a Nike Director or VP, there are many incentives for savings and investing through the Nike benefit programs. After making big decisions on your Deferred Comp, 401k deferral, and ESPP contributions, you may be left with decision fatigue when it comes to open enrollment for your health benefits.

Don’t let decision fatigue hinder you from taking advantage of the most underrated Nike benefit: the Health Savings Account (HSA).

Here are three reasons why you should consider implementing an HSA strategy for 2025.

1. HSA’s are the only account that is Triple Tax Advantaged

What does this mean?

Your contributions are tax-deductible.

Investment growth is tax-free.

Distributions are tax-free when used for qualified medical expenses.

That means that you never pay taxes at any point on these dollars. Think about all other Nike benefits and retirement accounts like your 401(k) and Deferred Comp plan, you only get two of these tax advantages and the IRS is getting their money at somewhere along the way. Using this strategy, you get to eliminate the IRS from the picture.

2. The Tax-Free Growth Opportunity

The goal of this HSA strategy is to save, grow and preserve these triple tax-advantaged dollars to be used for medical expense in retirement.

To do this correctly, you should contribute the maximum amount each year without taking distributions for medical expenses.

Prioritize using cash outside of your HSA account when medical expenses are incurred.

Next, do not leave the entire account balance in cash, but utilize the investment fund options so that you can capture the tax-free growth over the long-term.

Imagine a scenario where you were on the family HSA plan and contributed $8,550 per year for 5 years. You invested these funds and let them grow for 20 years until retirement, earning an average return of 8% per year. In 20 years, your HSA balance would be about $171,500 and you only contributed $42,750 to the account in the first 5 years. With rising health care costs, these funds can be used in retirement to pay for medical expenses, including Medicare premiums at age 65.

3. You own and control the account

Unlike Flexible Spending Accounts (FSAs) which are “use it or lose it” each year that you make contributions, the HSA is different because it’s an account that you own for your lifetime. You can keep the account if you change plans, retire, or leave Nike.

The contribution limits for 2025 are $4,300 for self-only coverage and $8,550 for family coverage. Those 55 and older can contribute an additional $1,000 as a catch-up contribution if not enrolled in Medicare. The contribution limits typically receive an inflation increase each year, so make sure you review this and stay up-to-date on the current amount.

Taxes can be one of the largest monthly expenses for many households. As a Nike Director or VP, you could be paying up to 51% in income taxes so it’s important to maximize every opportunity for tax savings.

To get the most benefit from your HSA, you need to be strategic, just as you would be when planning your Deferred Comp, 401k, and ESPP contributions. HSA’s are high deductible plans and if you anticipate substantial medical expenses, the HSA could cost you more than the lower deductible health plan options in 2025. This highlights why it’s important to evaluate the HSA as part of your comprehensive financial plan.

If you have questions about whether switching to the HSA is the right choice for you, please contact our team at nike@humaninvesting.com.