“Am I okay?” Fear ripe in my voice.

We just heard what no climber ever wants to hear: one loud scream, three thuds, then nothing.

At that moment, I was sixty feet in the air doing the routine work of cleaning the anchor, removing all the gear that protected us as we climbed up the route and re-setting the rope to be lowered and move on to the next climb when we heard it.

That sound? It was someone falling. Hard. We didn’t know how far or how badly, but we knew that climb was higher than mine: about eighty feet top to earth.

“I got you!” He called back. “Take a deep breath. Tell me what you’re doing.”

I did. I called out every single step I was taking to clean the anchor and secure the rope back to my harness –triple checked for safety – and he held the rope. Eventually, my feet and wobbling legs arrived safely back on earth.

When you rock climb, there is obvious risk involved. Risk that you accept as the price of admission for moving higher than twenty feet – the height where, if you fall, you most likely will not be fatally injured.

Confidence matters. Confidence in your gear, skill, weather, and your risk tolerance. Yet there is a confidence that is as important – if not more important – than all the confidence inside you: that is confidence in your belay partner.

Your partner is the one on the other end of the rope, your safety line, whose responsibility it is to pay attention, catch you when you fall, and lower you safely from sky to earth. A good belay partner must not only know the mechanics of climbing and safety but must also know you. They communicate clearly and are always paying attention – often mitigating the risks that are out of your control when you chose to leave the earth and head toward the open blue.

At no point after hearing those falling sounds did anything feel ok. My imagination was a wild hostage situation, forcing in front of my focus nightmares of gear failing and my body hurling through space.

But in reality, I was okay. I was safely anchored. We had a plan and practice in place for climbing safely. My belay partner was paying attention, “I got you”. He heard the sounds too, but he did not take his focus off the rope and my safety.

Investing in the stock market can be a lot like rock climbing

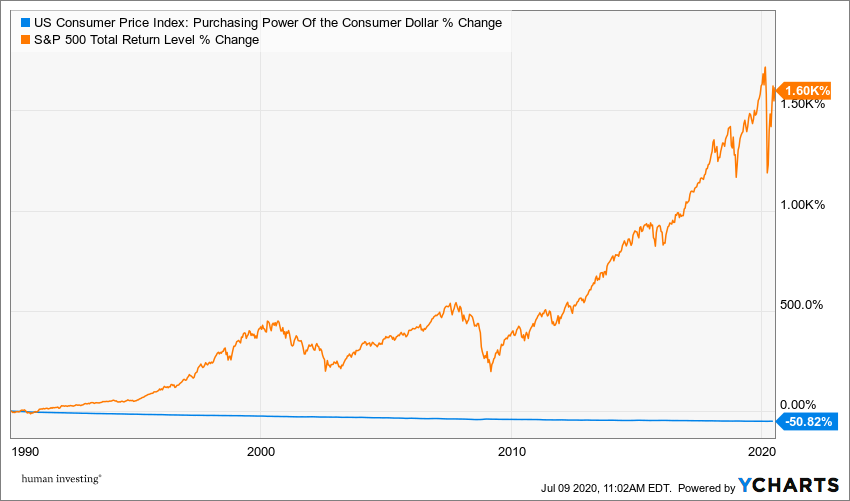

There is risk involved in climbing your portfolio value higher than a modest, though acceptable, goal of beating inflation.

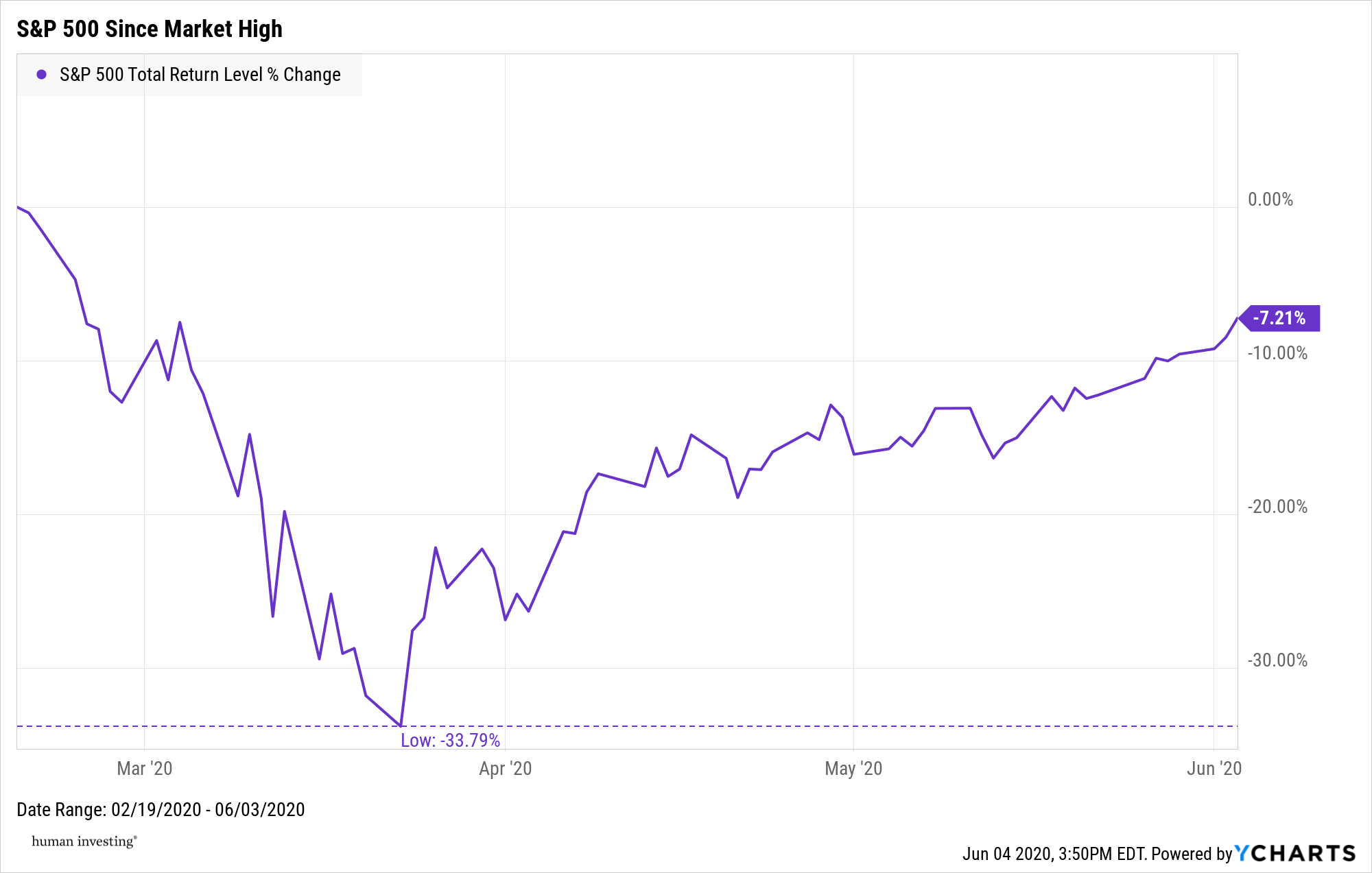

When the market takes a dive and the media heads are talking about total economic fall-out, it sure doesn’t feel okay. Do you have a good partner? A good advisor is a good partner.

Are they paying attention? When you hear the rumble and scary sounds of the market moving and you call out, “Am I okay?”, how does your advisor respond?

At Human Investing, we are your partner on the other end of the rope

Our climbing anchor is the fiduciary standard. Every trade, conversation, and piece of back-office work is done to mitigate unnecessary risk as your portfolio climbs, and it is all done with YOUR best interest in mind.

Our figure-eight is clean and tight. Your financial plan is like tying the climbing rope in to your harness – it is your safety line that serves to mitigate risk by informing how your dollars are invested to avoid and securely catch any falls. When the market crashes, we are on the other end of the line.

Our GriGri is loaded and locked. We have the highest standard in investment tools. We know our tools and we use them well, monitoring the “weather patterns” of the market, watching your portfolio as it climbs and responding as appropriate.

“On Belay? Belay on! Climbing? Climb on!” Before you climb you say to your partner: Are you ready and paying attention? We are paying attention and ready to serve you. There is more than one set of eyes on your accounts – you are more than dollars and stock holdings to us. We will not be distracted by the noise around us.

“I got you!” As with any good partner: We know you. We will respond to fear or a fall. Your time with us is invested in discussing your goals, your values, and your reactions when your portfolio climbs or lurches. We answer when you call, and sometimes we call you first because we also hear the sounds of the news and peers, and it may be scary. But in the end, we “got you.” We will not allow a fall-fear to inflict avoidable loss.

If you would like to talk to an advisor about how to climb your portfolio the Human Investing way, give us a call or send us an email. It would be our pleasure to partner with you.