The IRS adjusts tax brackets and rates each year to account for inflation and combat “bracket creep.” Bracket creep is when taxpayers are pushed into higher income tax brackets or do not receive adequate credits and deductions due to inflation. Are you aware of how an increase in the standard deduction and tax brackets will impact you?

What has changed?

1. The standard deduction will increase for the 2023 tax year. See below for a summary of the increases:

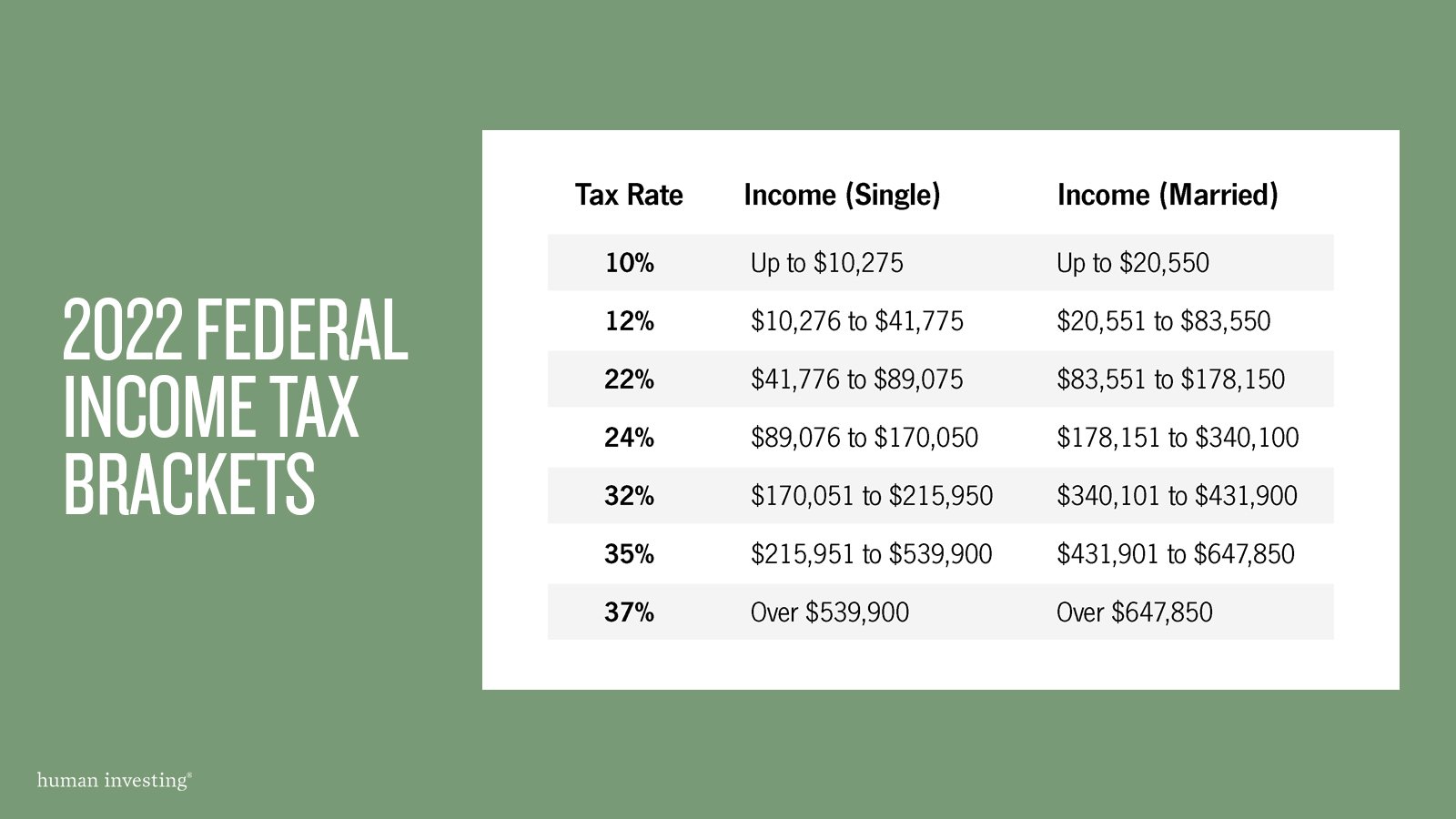

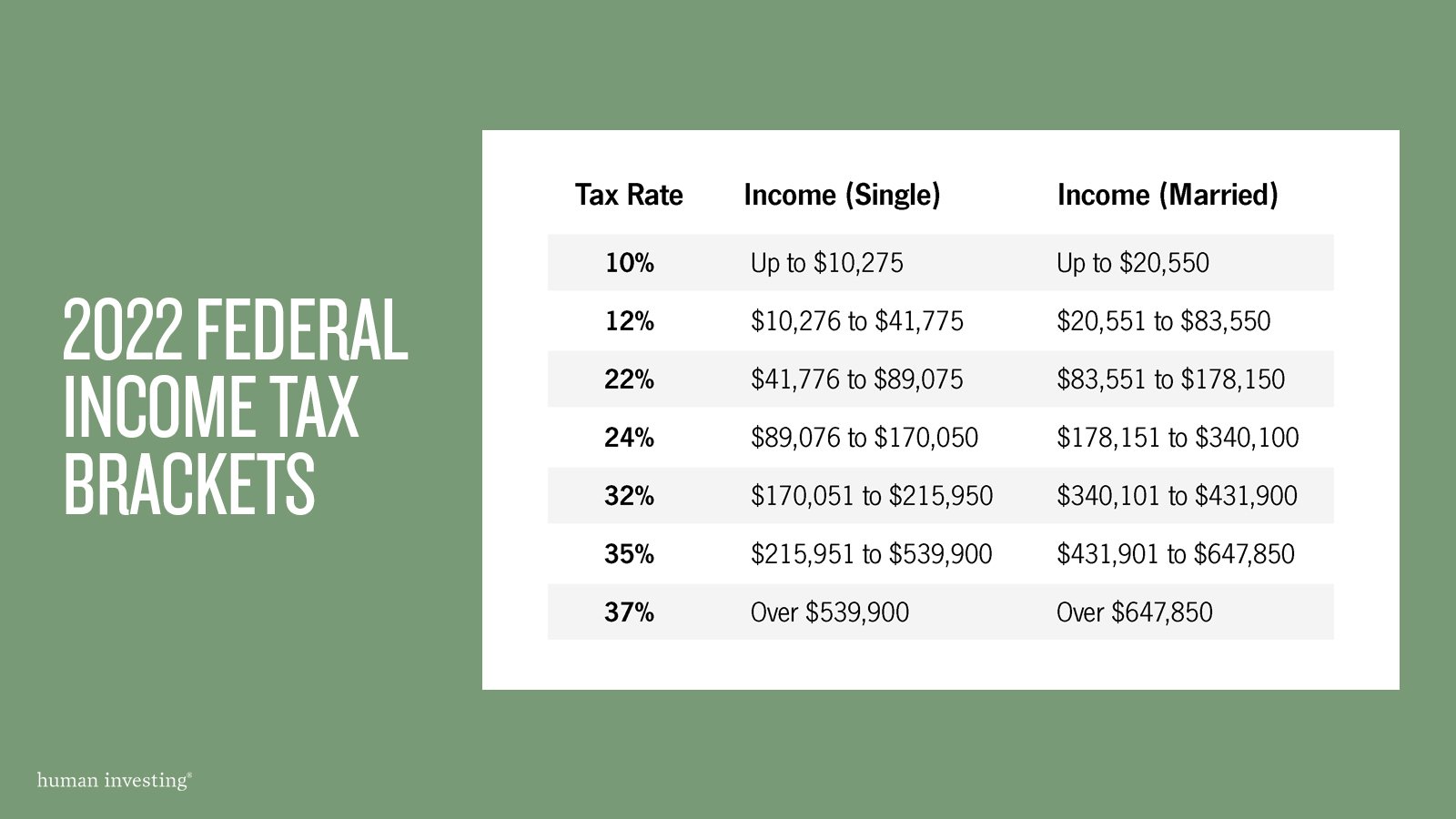

2. Federal income tax brackets will increase to account for inflation in 2023:

What does this mean for you?

While this is welcomed news, these updates will not significantly impact your taxes, cash flow, or budget. These updates are enacted to hedge against inflation and keep things consistent for taxpayers.

In sum, the increase in standard deduction means households will have less income subject to taxes, and the income subject to taxes will be subject to better tax brackets.

We wanted to re-vamp our tax example from 2022 with the updated 2023 numbers to provide a familiar and helpful guide to your taxes. Read on to see a fictitious example of the impact of the increased standard deduction and tax brackets in 2023.

Meet Martin & Angela

Below is a breakdown of their taxable income and taxes due in 2022 compared to 2023.

As you can see, they reported $100,000 of combined income, which is reduced by their pre-tax 401(k) contributions and the standard deduction of $27,700. Because the standard deduction increased from $25,900 in 2022 to $27,700 in 2023, Martin and Angela’s taxable income decreased. This means they are on track to pay less this year in federal taxes.

PORTIONS OF YOUR INCOME GET TAXED AT DIFFERENT RATES

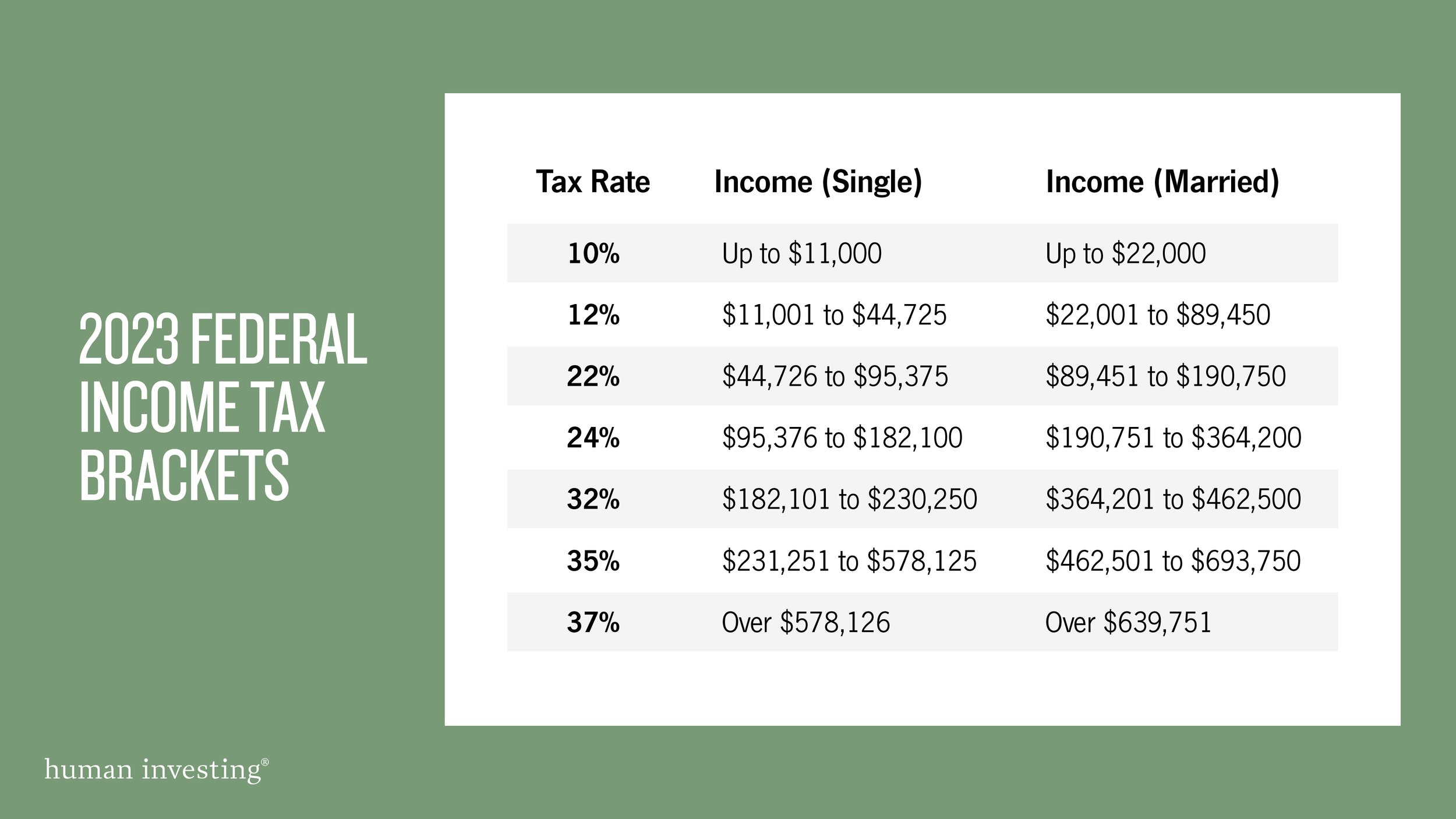

Tax brackets calculate the tax rate you will pay on each portion of your income. Tax brackets are part of our progressive tax system, which means the tax rate increases as someone’s income grows. There are seven federal tax brackets in 2023 (see image 2).

As shown in the image above, Martin and Angela’s taxable income will be split to take advantage of the lowest tax bracket. This means they will be taxed at 10% on the first $22,000 of their joint income, and their remaining taxable income will be taxed at 12%. In 2022, the maximum income allowed at the lowest tax bracket of 10% was $20,550. In 2023, the maximum income allowed will be $22,000.

If Martin and Angela fall into a higher tax bracket in the future, their taxable income will be broken down into each respective bracket to take advantage of the lower rates on what they can.

DRUMROLL, PLEASE…

After completing this exercise for all their taxable income, you can see that Martin and Angela’s total taxes owed in 2022 is $7,881 compared to $7,636 in 2023. This means they will pay $245 less federal taxes in 2023 than in 2022. While this is welcomed news, it is not a life-changing update.

If you have questions about your unique tax situation, please schedule a time to connect with our team. As always, we would love to hear from you!

Disclaimer: This post is for educational purposes and not predictive of your 2022 tax situation. The fictitious example is not a complete presentation of a tax filing.